Now that your kids have come along and your current house is getting cramped, you’re thinking of moving to a new home. There are so many lovely-to-live-in homes in Malaysia, particularly landed properties such as bungalows or Semi-Ds built amongst greenery or lifestyle-inspired condominiums factored with every imaginable facility built-in at hand. Every single one is perfect for your family. They are close to where you and your husband work, they are near the children’s schools, there are hospitals and banks and shopping malls as ─ but then there is one major dilemma:

Should you Buy or Rent?

Should you Buy or Rent? The traditional view is that one should always buy one’s own home because it is your investment property, it is the asset you can turn to as your education fund when your children are old enough for tertiary education, you can use them as rental property to seek rental returns, it can be your collateral to ask for funding should you decide to start your own business later on, or your retirement fund as part of your investment portfolio to add to your net worth. Finally it can even be passed on to your children as inheritance later on.

A lot of parents buy property for their children to secure their futures for later life.

These are all the pros of buying your own property but then, there are cons as well and they include having to make a major commitment in life to fork out a huge sum every month, come what may, for the next 25 to 35 years non-stop.

Renting might be better. You get all the perks without the huge upfront outlays, the do-or-die commitment and you won’t have the noose of your loan provider hanging around your neck all the time ─ (read: miss one loan repayment and they’ll threaten to auction off your house, sometimes with you still in it).

That said, let’s take a look at whether renting or buying is better.

Buying Your Own Home

The Benefits:

1. You Get Autonomy Over Your Own Abode

Feel like adding a balcony to the side of the house or changing the kitchen cabinets or knocking down a room wall to make the upstairs family space bigger?

Go ahead. It’s your home, do what you like.

2. It’s an Investment that will Grow to Benefit Your Future

It’s a great investment which will become your nest egg for the future in any way you want to use it. Again it’s back to autonomy. You can decide to live in it, rent it out or sell it off and make a profit or even remortgage later on in life when you need to borrow a loan. You never know what the future will bring or when you may need to convert your asset to cash.

3. You can Avoid Living Under the Rules of the Landlord

Woe betide you if you get a fussy landlord. Some landlords come over to check their homes just to see that you haven’t done anything untoward to his precious property. If and when there are repairs to be done ─ some landlords will be very reluctant to say, repair a leaking roof or change a broken piping or even add ceiling fans. You would have to negotiate and renegotiate and he may take months to see to your complaints. And don’t you ever be late with the rent lest you find yourself in the streets after an eviction order.

Some landlords don’t want young children or pets (if you have any) renting their houses as they fear the former and latter may mess up the premise.

The Pitfalls:

1. You’ll have to Cough Up a Very Large Sum of Money Upfront

The downpayment of 10% of the price of the house is where buyers usually balk at. If you’re looking at at RM50,000 house, you’d have to cough up RM50,000 upfront. And then there is the price of the Sales and Purchase Agreement (SPA), your Stamp Duty for Transfer of Ownership Title (MOT), plus lawyer’s fees including from your loan bank called Loan Facility Agreement fees, Mortgage Reducing Term Insurance, bank processing fee etc etc etc, not to mention other expenses such as moving cost, furniture, fittings, renovation and so on and so forth.

After the loan bank approves the loan, you’d have to start paying your monthly mortgage for the rest of your life. Some loan tenures are as long as 30 years. The longer the tenure, the less you pay but the longer it will drag until it becomes unbearably tedious.

For a standard home loan, the current market rate now is around 4.5% to 4.6% p.a. interest depending on the bank. The interest rate is based on the Base Rate or Base Lending Rate of Bank Negara Malaysia. That means for a RM50o,000 home of which you have just paid RM50,000 as downpayment, you’ll have to pay at least RM2,280 a month for the next 30 years of your life. Can you keep this up?

If you have bought an apartment or condominium, don’t forget you have to pay maintenance fee and contribute to the sinking fund on top of your monthly mortgage installments.

2. It’s a Big Financial Risk

Although it is generally said that properties appreciate over time, that saying may not hold true for all properties. Some townships never materialize despite what was touted on paper at the point of sale. Some projects have defects which may never get resolved (such as land subsidence and crack in the wall depreciating the value of your property). Some projects get abandoned halfway. Some locations suddenly depreciate in value. What then are you left with?

3. You Make a Scary, Lifelong Commitment

Can you guarantee you will have a job with an ascending salary scale over the next 20 to 30 years of your life. Or how about, can you guarantee you will have a job in the first place and always have the money to service your mortgage?

4. Stuck for Good

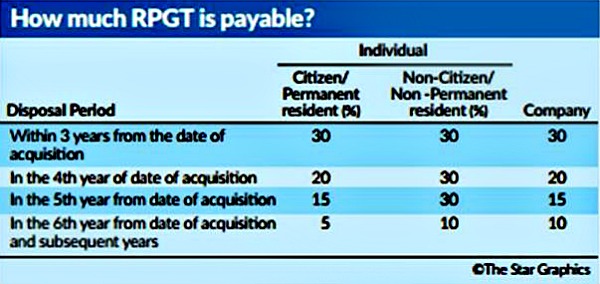

The value of a piece of property rises over time. What if you don’t like your neighbours or neighbourhood one year after you move in. The roads may get too crammed with neighbours’ cars, or your neighbourhood could have robberies and pose a security issue or a new neighbour moves in and makes life hell for you. What can you do? You can’t move as you like as then you’d have to pay rent for your new home and service a mortgage for your old home and you can’t sell off your property too fast lest you get hit by RPGT.

What is RPGT? It’s Real Property Gains Tax which is tax imposed on property sold off within the first five years of purchase. Effective Jan 1, 2019, the RPGT has been increased for disposal of a property from the sixth year onwards. The table below is a summary of the RPGT rates.

Renting Your House

The Benefits

1. You Can Be a Mobile Millennial Mum and Move

If you don’t like the place or you are bored with it or it has become too cluttered for your family or you don’t like your neighbours ─ just move! It’s as simple as that. You can even break your tenancy agreement, so long as you inform your landlord and come to an understanding, and get on with moving on with your new life in a new home.

2. Your landlord Covers All Maintenance Costs

You are paying rent so your landlord is supposed to ensure everything is in tiptop condition for your tenancy there. Furthermore, some rental homes come fully-furnished. You need only bring your luggage and everything else is set out for you. Thereafter, you need only pay your monthly rent and utilities to enjoy the premises.

3. Lower Upfront Fees, More Cash Flow in the Household

Sure, you may have to pay 2+1 (three months rental) upfront before you can move in. These are the standard rates for renting but this upfront amount comes nowhere near to what you would have to cough-up when buying your own piece of property. Rental fees are usually lower than mortgage. This means you would have more cash flow to use for your daily expenses. When having children to bring up, this extra cash can come in very, very handy.

The Pitfalls:

1. Not Getting a Return on All That Money Spent

Unlike owning a property where you get a piece of real estate at the end of day, you pay your rent and it goes up in smoke. Rent a place for 10 years and at the end of the day, you come back empty handed. What has happened is that you have essentially paid up the mortgage of the house for the landlord.

2. Your Rent Could Suddenly Rise

There is no legal framework that protects tenants in Malaysia. Although there is a market rate and landlords charge rental fees accordingly, your rent can suddenly increase, unlike fixed-rate mortgage due to spikes in location value. You also could find yourself being asked to vacate the premise because the owner has decided to sell off the property or take it back for himself.

3. You Can’t Do As You Please to the House

If the home doesn’t suit your family, the corridors are too narrow, the kitchen is too small or the yard cannot accommodate the washing and drying, there’s not a thing in the world you can do about it. Live with it and forever hold your peace ─ until you decide to move out that is.

[dropcap letter=”F”]ortunately, there are such things as Rent-to-Own Schemes in Malaysia which tries to bridge the dichotomy between renting or buying. Now you can have both but that will be covered in the next topic in Motherhood.com.my