In the last article on housing for families in Malaysia, Rent To Own (RTO) schemes may be the answer to bridge the chasm between buying or renting.

Every family looking for a roof over their heads faces this problem at some point in their lives. If you rent, you lose out in the end because you have paid a massive sum in rentals over the years only to benefit your landlord. He gets his house paid by you while you, at the end of the day, come away with nothing. On top of that, you will always be paying for a roof over your head if you choose to pay rent for the rest of your life.

If you buy, you can rest assured that one day, at the end of your mortgage tenure, you will not have to pay a single sen more for that roof over your head. Your home will finally belong to you, you will live in a “free-to-occupy” home for as long as you live and your name will be emblazoned on the Deed as proud owner of a valuable piece of real estate. Sounds hunky dory?

Well, the journey there is never paved with roses. The biggest impediment is the cost, or specifically the downpayment of 10% of the price of the home, whether you buy subsale or new. For a RM300,000 home for instance, the 10% would be a whopping RM30,000 upfront, not inclusive of other payments such as the price of the Sale and Purchase Agreement (SPA), Stamp Duty, Loan Facility Agreement fees and yada yada. This additional cost could work out to be in the tens of thousands of your initial 10%.

Heads Up On A Hidden Expense

Another hidden cost that is never mentioned anywhere but certainly experienced by house buyers in Malaysia is the penalty you would have to pay for late disbursement of the loan amount from your loan bank into the seller’s or developer’s account. A simpler explanation would go like this: You are borrowing from Bank B to put the sum of the house you have bought into Bank A (the seller’s bank). Usually after signing the SPA, you have a set number of days to settle the balance. However Bank B, for whatever reason, may take up to six months or more to disburse those funds into Bank A. You, the borrower, meanwhile, will pay the penalty of lateness to Bank A even though it is not your fault at all. But those are the rules of the game and it has been going on silently for years. The penalty for every day of delay can come up to hundreds of Ringgit depending on the price of the house. Imagine paying RM500 to thousands every month for late charges not caused by you?

Admittedly it doesn’t happen to everyone but quite a few house buyers have walked this road. The path to buying property is therefore laden with hidden potholes; it’s mostly to do with money and is the first barrier that bars most people from owning their own home.

And yet, in Malaysia, lots of families ─ mums and dads ─ are looking to own their first home.

Rent To Own ─ What is it?

Given the many house-renting or buying problems, Malaysia introduced the Rent To Own scheme as far back as 2014. It is not an original or new-fangled idea. In fact, the first Rent To Own schemes began in the United Kingdom, Europe and the United States in the 1950s and 1960s.

Malaysia adopted the practice as 1Malaysia People’s Housing Programme (PR1MA) that allowed tenants the option to buy the rented property after five or 10 years at a predetermined price.

Fastforward to today and it looks like Rent To Own in Malaysia is becoming popular. Already many developers have launched variants of the scheme calling it “Reside and Purchase”, “Stay Now and Buy Later” and so on.

On the financial institution front, Maybank Islamic launched HouzKEY in November 2017. It was the first bank in the nation to offer this facility.

The scheme has gathered momentum and is rolling across the states in the country with Selangor being the first to see widespread adoption for its properties. In fact, it was reported at the end of last year that Zuraida Kamaruddin, Housing and Local Government Minister had said Rent To Own would be further expanded nationwide. In April 2019, it was reported in the Edge Markets that foreign agencies in countries like China, China, South Korea and the Middle East have expressed interest in financing Malaysia’s Rent To Own schemes.

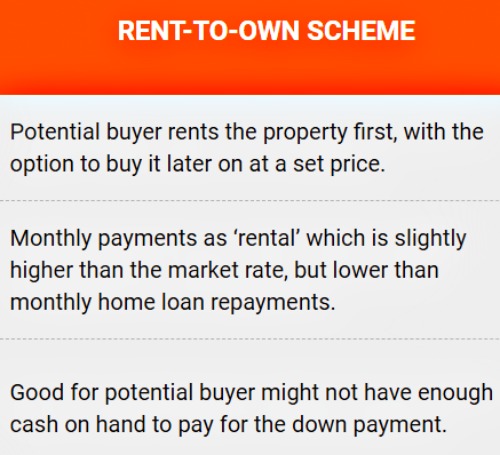

How Does Rent To Own (RTO) Work?

Essentially, the scheme works on a try-before-you-buy principle. You sign a rental lease which gives you the option of buying in the end. It’s a win-win situation, especially for young families still trying to sort out their finances. The tenant doesn’t lose out on paying for nothing and could have a property of his or her own without having to fork out the hefty sum required upfront if they went and bought the property outright.

1. Who is Eligible To Apply?

Malaysian citizens or permanent residents of Malaysia aged 18 onwards. Guarantors from own family members are allowed and encouraged.

2. How to Apply?

To apply, buyers need to pin down the property they are interested, check if they are participating RTO properties and submit the relevant documents.

3. How much Monies Needed?

Upon approval successful applicants and their guarantors will have a set number of days (usually seven) to pay the three-month rental as security deposit and sign the lease agreement. Therefore you need three month’s rent to qualify, and not 10% of the house price.

4. How long is the Lease-Purchase period?

Depending on who you entered the contract with, this might be five to 30 years. At the end of this contract, you can exercise the option to purchase the property. At HouzKEY for example, the contract period runs for a minimum of five years, with an option to renew every three years for a maximum of up to 30 years.

Rental for the first five years will be fixed at a flat rate, but should the tenant decide to go for the renewal option, there will be an annual 2% increase in the rent. After servicing a 12-month rental period, tenants can choose to exercise the option to purchase by migrating to a mortgage facility.

5. Whats’s the Good and Bad of RTO?

Good:

The property price is locked from day one and the rental amount paid will reduce a portion of the property price, opening the possibility of owning that property minus the 10% deposit, legal fees and all those hefty sums.

Bad:

The property is not yours during the lease period for however long you have signed up for. This means you can’t renovate or make any changes without the owner’s approval. In the unlikely event that property prices drop, you won’t be able to buy at the cheaper rate. Since you locked the price in based on its value at the point of purchase, you’ll have to buy at the price that was originally agreed to.

[dropcap letter=”H”]ouzKEY and PR1MA are not the only ones offering RTO. As mentioned earlier, many developers in Malaysia have started offering their own variations of the RTO scheme. Terms and conditions vary. So if you do see a home proffered by them that you would like to try out, do ask them about their scheme.

For more stories on smart parenting ,and finances visit Motherhood.com.my